Graphics processing items (GPUs) are the principle knowledge heart chips utilized in synthetic intelligence (AI) growth. The finest GPUs within the business are provided by Nvidia and Advanced Micro Devices, and each of these firms supply an vital part referred to as high-bandwidth reminiscence (HBM) from Micron Technology (MU 6.74%).

Micron’s HBM options are fitted alongside superior GPUs, the place they preserve knowledge flowing seamlessly to unlock most processing speeds. The firm is experiencing astronomical demand proper now, which is driving a surge in its income and earnings. As a end result, its inventory has gained a whopping 323% during the last 12 months alone.

But can the blistering returns proceed?

Image supply: Getty Images.

Memory is crucial for processing AI workloads

GPUs want a continuing stream of knowledge when coaching AI fashions and serving them to end-users. HBM shops this knowledge in a prepared state for when the GPU wants it, and the upper the reminiscence capability, the extra knowledge it could maintain within the pipeline. Conversely, a low reminiscence capability would result in bottlenecks, forcing the GPU to pause its workloads whereas it waits to obtain contemporary knowledge.

Micron’s HBM3E answer for the information heart affords 50% extra capability than the competitors, whereas consuming 30% much less vitality. This is a successful mixture for AI builders who need the quickest processing speeds and the bottom potential value.

But Micron will ramp up manufacturing of its new HBM4E answer this yr, which is able to ship a whopping 60% extra capability than HBM3E, whereas consuming 20% much less vitality. It is predicted to energy Nvidia’s new Vera Rubin chips, which would be the strongest on the earth for AI workloads after they enter mass manufacturing within the second half of 2026.

Micron’s total 2026 provide of knowledge heart HBM is already utterly bought out, however its alternative is simply simply ramping up. This market was value $35 billion in 2025, and the corporate says it may develop by 40% per yr till 2028, reaching $100 billion.

March 18 may very well be an important day for Micron

Micron wrapped up its fiscal 2026 second quarter on the finish of February, and it is scheduled to report its working outcomes for the interval on March 18. Based on administration’s steerage, the corporate’s whole income probably got here in at a file $18.7 billion, which might be a whopping 132% from the year-ago quarter. That could be a major acceleration from the 56% progress it produced within the first quarter, simply three months earlier.

Micron’s cloud reminiscence phase (the place it stories knowledge heart HBM gross sales) was the star of the present within the first quarter, with income practically doubling yr over yr to $5.3 billion. I might count on a good stronger end result on March 18, primarily based on administration’s general top-line forecast.

The different massive factor to observe on March 18 is Micron’s earnings, that are anticipated to blow up greater by 480% yr over yr to $8.19 per share. As was the case with the highest line, this is able to even be a significant acceleration from the 175% progress the corporate produced within the first quarter.

Earnings drive inventory costs, so this quantity — together with administration’s forecast for the subsequent quarter — may dictate whether or not additional good points are forward for Micron shareholders.

Today’s Change

(-6.74%) $-26.75

Current Price

$370.30

Key Data Points

Market Cap

$417B

Day’s Range

$367.45 – $391.18

52wk Range

$61.54 – $455.50

Volume

77K

Avg Vol

34M

Gross Margin

45.53%

Dividend Yield

0.12%

How a lot greater can Micron inventory go from right here?

The semiconductor business has all the time been very cyclical, which means firms would spend some huge cash to construct infrastructure after which pull again for a number of years, till it was time to improve. AI has shortened that improve cycle to 12 months — or much less in some instances — so knowledge heart operators are repeatedly spending cash.

In truth, Nvidia CEO Jensen Huang believes knowledge heart operators will likely be spending as much as $4 trillion per yr on AI infrastructure by 2030 to satisfy demand for cloud computing capability from builders. Plenty of that spending will stream to chipmakers, and if you happen to imagine Nvidia will proceed promoting truckloads of GPUs, then it is solely logical to be bullish on Micron’s enterprise, given HBM is such a key piece of the puzzle.

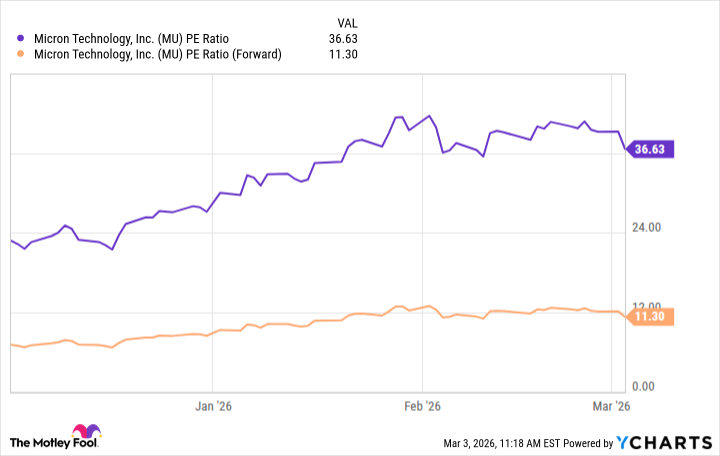

Based on Micron’s trailing 12-month earnings of $10.52 per share, its inventory is buying and selling at a price-to-earnings (P/E) ratio of 36.6, which is nearly precisely in keeping with Nvidia’s P/E. From that perspective, one may argue Micron might be pretty valued.

But here is the place issues get fascinating. Wall Street’s consensus estimate (offered by Yahoo! Finance) suggests Micron’s full-year fiscal 2026 earnings will are available at $34.16 per share, inserting its inventory at a ahead P/E ratio of simply 11.3.

Data by YCharts.

That means the inventory must rocket greater by one other 223% over the subsequent six months alone simply to keep up its present P/E ratio of 36.6.

I’m not suggesting that can occur, as a result of there are actually dangers on the horizon. For instance, main start-up OpenAI lately stated it’s going to scale back its deliberate infrastructure spending between now and 2030 to $600 billion, from $1.4 trillion beforehand. If this turns into an industrywide phenomenon, then Huang’s forecast is perhaps too formidable.

Nevertheless, there may be actually room for upside in Micron inventory as issues at present stand. It may not triple over the subsequent six months, however I will not be shocked if it is buying and selling a lot greater.